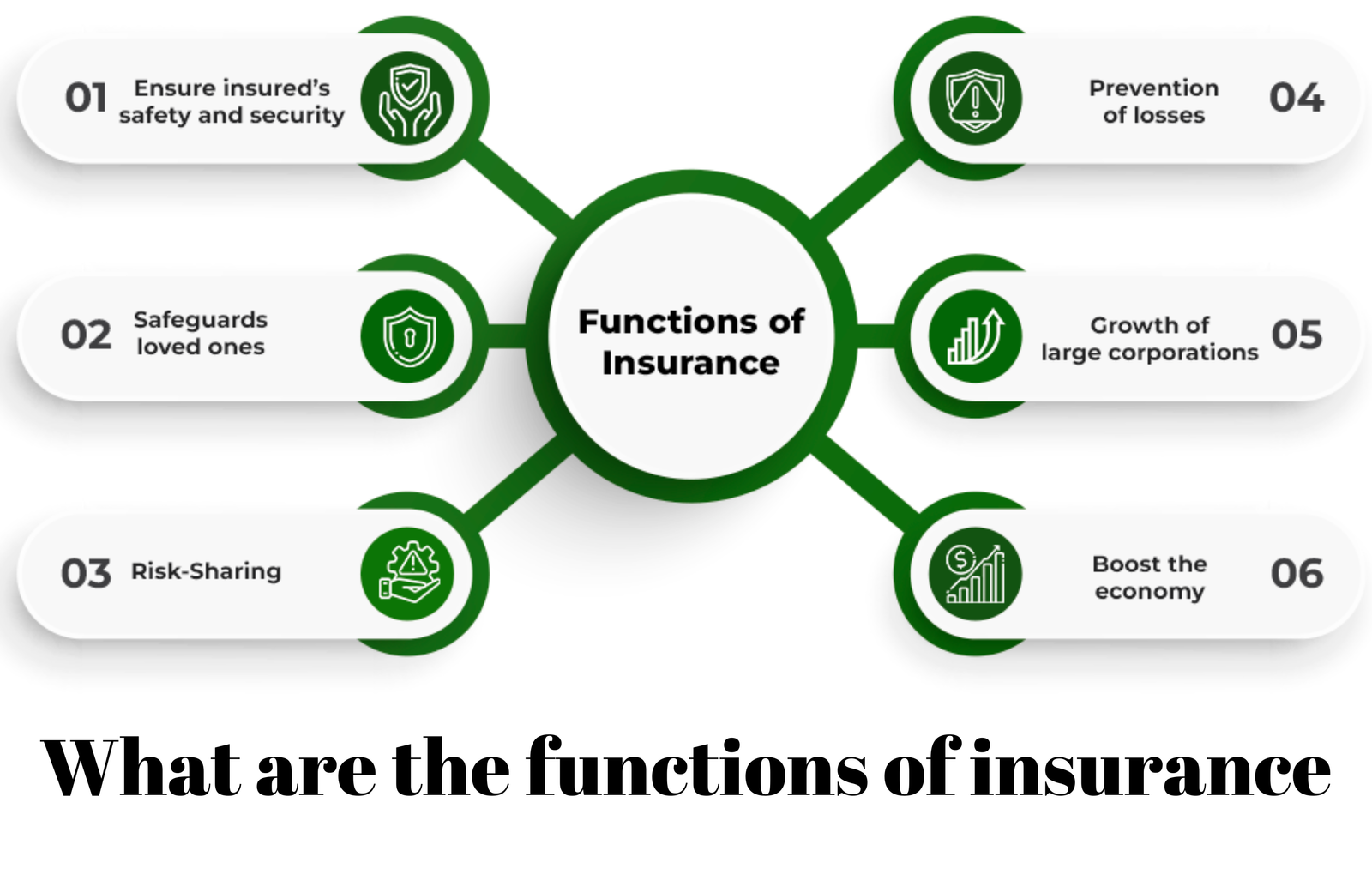

What are the functions of insurance

Definition of Insurance

Insurance is a financial arrangement in which an individual or entity (the insured) pays a premium to an insurance company (the insurer) in exchange for protection or coverage against specified risks. In the event of a covered loss, the insurer provides compensation or benefits to the insured according to the terms and conditions outlined in the insurance policy. The fundamental principle of insurance is to spread the risk of loss among a large pool of policyholders, thereby reducing the financial impact of unforeseen events on any single individual or entity.

Historical Evolution

The historical evolution of insurance spans thousands of years, with its roots dating back to ancient civilizations. Here’s a brief overview:

a. Ancient Practices:

Some of the earliest forms of risk transfer and mutual aid can be traced back to ancient civilizations such as Babylonia, China, and Rome. Merchants and traders formed agreements to protect against losses from theft, shipwrecks, and other perils.

b. Medieval Guilds:

In medieval Europe, guilds and trade associations provided a form of mutual insurance to their members. Members contributed to a common fund that would be used to compensate individuals for losses such as fire damage or theft.

c. Marine Insurance:

Maritime trade in the Middle Ages led to the development of marine insurance. Merchants and shipowners pooled their resources to protect against the risks of transporting goods across oceans. Lloyd’s of London, founded in the late 17th century, became a prominent center for marine insurance.

d. Modern Insurance Industry:

The modern insurance industry began to take shape in the 17th and 18th centuries. Insurance companies emerged in Europe, offering coverage for various risks including fire, life, and property damage. The first life insurance policy is believed to have been issued in the early 18th century.

e. Actuarial Science:

The development of actuarial science in the 19th century revolutionized the insurance industry. Actuaries used statistical methods to analyze risk and calculate premiums more accurately, leading to the expansion of insurance products and the growth of the industry.

f. Regulation and Standardization:

In the late 19th and early 20th centuries, governments began to regulate the insurance industry to protect consumers and ensure the financial stability of insurers. Regulatory bodies were established to oversee insurance operations and enforce industry standards.

Importance in Modern Society

Insurance plays a crucial role in modern society for several reasons:

1. Risk Management:

Insurance provides individuals, businesses, and governments with a mechanism to manage various types of risks, including property damage, liability claims, illness, disability, and loss of life. By transferring the financial consequences of these risks to insurers, individuals and organizations can protect themselves against potentially catastrophic losses.

Understanding Risk:

Understanding risk is essential in the context of insurance and broader financial decision-making. Here are the key aspects involved:

- Definition of Risk: Risk refers to the uncertainty of outcomes and the potential for adverse or unexpected events to occur. It encompasses the possibility of both positive and negative outcomes, with varying degrees of probability and impact.

Types of Risk:

-

- Pure Risk: Involves the possibility of loss or harm without the opportunity for gain. Examples include natural disasters, accidents, illness, and death.

- Speculative Risk: Involves the possibility of both gain and loss, such as investment risk or business ventures. Unlike pure risk, speculative risk presents the opportunity for profit alongside the potential for loss.

Risk Factors:

-

- Frequency: The likelihood or probability of a specific risk event occurring within a given time frame.

- Severity: The potential magnitude or impact of a risk event, often measured in terms of financial loss, physical harm, or other adverse consequences.

- Duration: The length of time over which a risk exposure persists or remains relevant.

- Correlation: The degree to which different risks are related or move in tandem with one another. Understanding correlations helps assess the diversification benefits of combining multiple risk exposures.

Risk Assessment:

-

- Identification: The process of identifying and understanding potential risks, including their causes, consequences, and contributing factors.

- Analysis: The evaluation of risk exposures in terms of their likelihood, impact, and interdependencies. This may involve quantitative techniques such as statistical modeling or qualitative methods such as scenario analysis.

- Prioritization: The ranking of risks based on their significance, allowing resources to be allocated effectively to address the most critical exposures.

Risk Management:

-

- Mitigation: The implementation of measures to reduce the likelihood or impact of identified risks. This may include preventive actions, risk transfer mechanisms (e.g., insurance), or contingency planning.

- Transfer: The transfer of risk to another party, such as an insurance company, in exchange for a premium. Insurance allows individuals and organizations to transfer the financial consequences of certain risks to a specialized risk bearer.

- Retention: The acceptance and retention of risk exposure within an organization’s tolerance levels. Retention strategies may involve self-insurance, reserve funds, or risk acceptance based on a cost-benefit analysis.

Risk Identification:

Risk identification is the process of systematically identifying, describing, and documenting potential risks that could affect an organization, project, or activity. Here’s a structured approach to risk identification:

Establish Context: Understand the objectives, scope, stakeholders, and other relevant factors of the project or activity for which risks need to be identified.

Gather Information:

Collect relevant data, documentation, and insights from various sources, including:

-

- Project plans and schedules

- Previous similar projects or activities

- Stakeholder input and expertise

- Industry best practices and standards

- Regulatory requirements

- External environmental factors (e.g., market conditions, geopolitical events)

Brainstorming and Workshops:

- Conduct brainstorming sessions or workshops with relevant stakeholders to generate ideas and insights about potential risks. Encourage open communication and diverse perspectives to uncover a wide range of risks.

Risk Categories:

- Use predefined categories or classifications to organize and structure the risk identification process. Common categories include:

- Strategic risks

- Operational risks

- Financial risks

- Compliance risks

- Reputational risks

- Technological risks

- External risks (e.g., regulatory changes, market fluctuations)

Checklists and Templates:

- Utilize checklists, templates, or risk registers to systematically review different aspects of the project or activity and identify potential risks. These tools can help ensure comprehensive coverage of all relevant risk areas.

SWOT Analysis:

2. Conduct a SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis to identify internal and external factors that could impact the project or activity. The “Threats” component of SWOT analysis specifically focuses on identifying risks.

Root Cause Analysis:

3. Analyze past incidents, failures, or near-misses to identify underlying causes and contributing factors that could lead to similar risks in the future. Root cause analysis helps uncover systemic issues that may otherwise go unnoticed.

Risk Assessment

Risk assessment is the process of evaluating and analyzing identified risks to determine their likelihood, potential impact, and overall significance. It involves quantifying and qualitatively assessing risks to prioritize them for further management actions. Here’s how the risk assessment process typically unfolds:

Risk Identification:

Before conducting a risk assessment, it’s essential to identify and document potential risks that could affect the objectives, projects, or activities of the organization. This step ensures that all relevant risks are considered during the assessment process.

-

Risk Analysis:

- Likelihood: Assess the probability or frequency with which a risk event might occur. This assessment can be based on historical data, expert judgment, statistical analysis, or predictive modeling.

- Consequences: Evaluate the potential impact or severity of the risk event if it were to occur. Consider both the direct and indirect consequences on various aspects such as financial, operational, reputational, legal, and safety.

- Vulnerability and Resilience: Consider the organization’s vulnerabilities and resilience factors that may influence the likelihood and consequences of risks. Factors such as the effectiveness of existing controls, redundancies, and response capabilities can affect the overall risk profile.

-

Risk Rating:

- Combine the assessments of likelihood and consequences to assign a risk rating or score to each identified risk. This rating helps prioritize risks based on their significance and informs decision-making regarding risk management strategies.

- Common methods for risk rating include using risk matrices, risk scoring models, or probabilistic analysis techniques.

-

Risk Prioritization:

- Prioritize risks based on their ratings to focus resources and attention on managing the most significant threats first. Risks with higher likelihood and impact ratings typically receive greater priority for mitigation or response efforts.

- Consider additional factors such as strategic importance, regulatory requirements, stakeholder concerns, and resource constraints when prioritizing risks.

-

Risk Treatment:

- Develop and implement risk treatment strategies to manage and control prioritized risks effectively. Depending on the nature of the risks, treatment options may include risk avoidance, risk mitigation, risk transfer, or risk acceptance.

- Establish clear action plans, responsibilities, timelines, and performance metrics for implementing risk treatments.

Financial Protection:

Insurance provides financial protection and peace of mind to policyholders by offering compensation or benefits in the event of covered losses. This protection can help individuals and businesses recover from unexpected events such as natural disasters, accidents, or illnesses without suffering severe financial hardship.

Promoting Economic Stability:

Insurance contributes to economic stability by spreading the financial impact of losses across a large pool of policyholders. In the aftermath of disasters or large-scale events, insurance payouts help individuals and communities rebuild and recover, minimizing the negative effects on the economy.

Facilitating Investment and Innovation:

Insurance companies play a vital role in facilitating investment and innovation by providing a safe and stable environment for individuals and businesses to take risks. Insurers help entrepreneurs and innovators mitigate the financial risks associated with new ventures, encouraging investment in research, development, and entrepreneurship.

1 thought on “What are the functions of insurance”