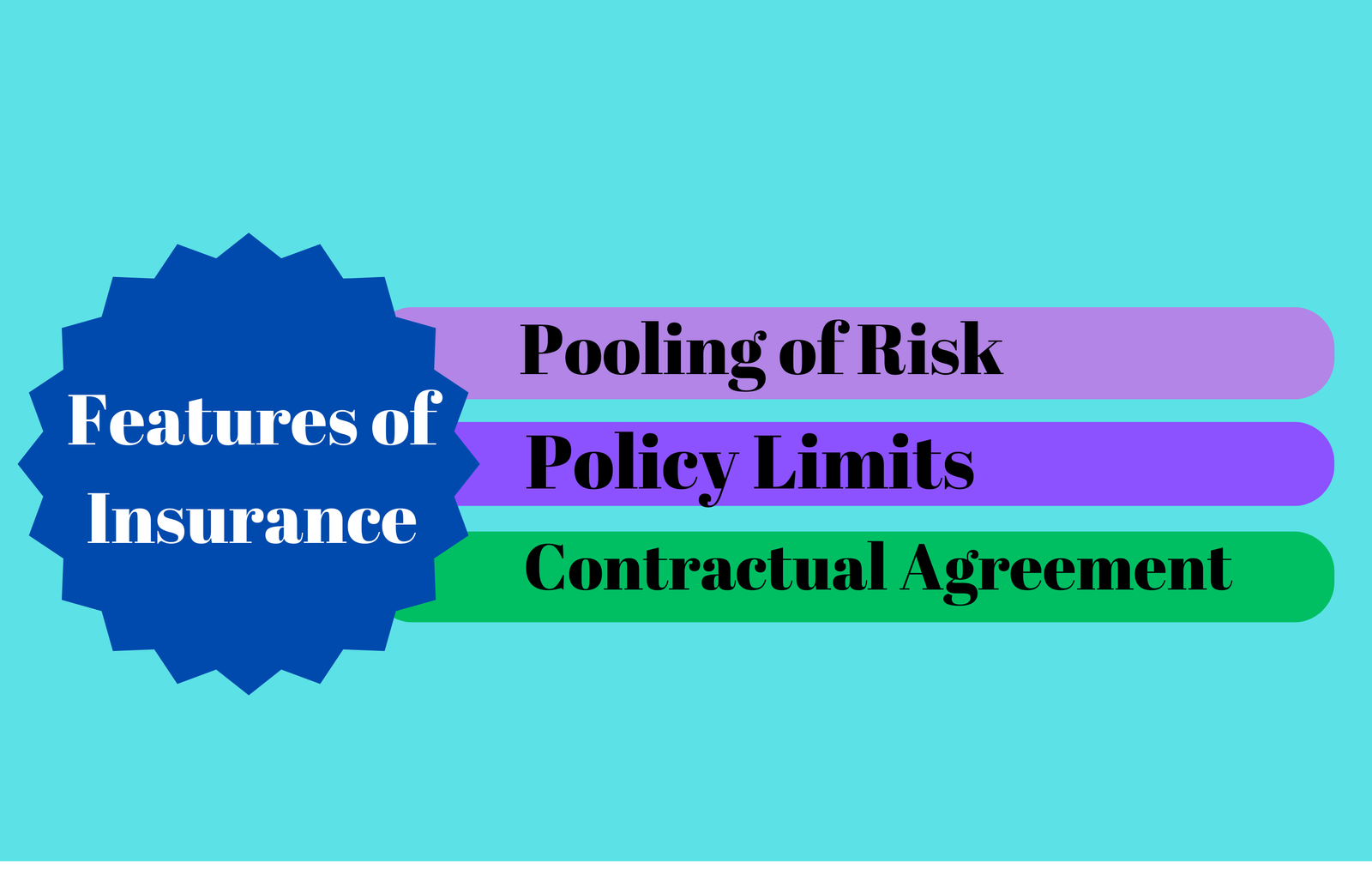

The main features of insurance include:

-

-

Pooling of Risk:

Insurance works on the principle of pooling risk among a large group of policyholders. Premiums paid by policyholders are pooled together to cover the losses of those who experience covered events.

2. Financial Protection:

Insurance provides financial protection against unforeseen events or risks, such as accidents, illnesses, natural disasters, or property damage.

3. Indemnification:

Insurance policies typically provide indemnification, which means that the insured party will be compensated for covered losses or damages up to the policy limits, helping them recover financially from the loss.

4. Contractual Agreement:

Insurance operates based on a contractual agreement between the insured and the insurer. The policy outlines the terms, conditions, coverage limits, and exclusions of the insurance arrangement.

5. Premiums:

Policyholders pay premiums to the insurer in exchange for coverage. Premiums are typically paid regularly (e.g., monthly, quarterly, annually) and are determined based on factors such as the level of risk, coverage amount, and the insured’s profile.

6. Policy Limits:

Insurance policies often have limits on the amount of coverage provided for different types of losses. Policyholders need to be aware of these limits to ensure they have adequate coverage for their needs.

7. Exclusions:

Insurance policies may include exclusions, which are specific events or circumstances not covered by the policy. Policyholders need to understand these exclusions to avoid misunderstandings during claims processing.

8. Risk Transfer:

Insurance allows individuals or organizations to transfer the risk of financial loss from themselves to an insurance company in exchange for payment of a premium.

-

Types of Insurance

Life Insurance

When purchasing life insurance, individuals should consider factors such as their financial obligations, the income needs of their dependents, future financial goals, and budgetary constraints. It’s essential to review policy terms, coverage options, premiums, and riders (optional features) to select the most suitable life insurance policy for their needs.

Life insurance is a contract between an individual (the policyholder) and an insurance company, where the insurer agrees to pay out a sum of money (the death benefit) to designated beneficiaries upon the death of the insured person. The purpose of life insurance is to provide financial protection to the insured’s loved ones or dependents in the event of their death.

There are several types of life insurance policies, but the two main categories are:

1. Term Life Insurance:

This type of policy provides coverage for a specific period, such as 10, 20, or 30 years. If the insured dies during the term of the policy, the beneficiaries receive the death benefit. Term life insurance does not typically accumulate cash value, and premiums are generally lower compared to other types of life insurance.

2. Permanent Life Insurance:

Permanent life insurance provides coverage for the entire life of the insured, as long as premiums are paid. This category includes various types of policies, such as whole life insurance, universal life insurance, and variable life insurance. Permanent life insurance policies often include a cash value component, which accumulates over time and can be accessed by the policyholder through withdrawals or loans while they are alive.

Life insurance can serve multiple purposes, including:

-

- Income Replacement: Life insurance proceeds can replace lost income and support the financial needs of the insured’s dependents, such as paying for living expenses, mortgage payments, or educational expenses.

- Debt Repayment: Life insurance can be used to pay off debts, such as mortgages, personal loans, or credit card balances, ensuring that the insured’s loved ones are not burdened with financial liabilities.

- Estate Planning: Life insurance proceeds can be used to provide liquidity for estate taxes or to equalize inheritances among beneficiaries.

4. Business Continuity: Life insurance can be a crucial component of business succession planning, providing funds for the purchase of a deceased owner’s share of a business or compensating for the loss of key personnel.

Health Insurance

Health insurance is essential for protecting individuals and families from the potentially high costs of healthcare services and ensuring access to necessary medical care when needed. It’s important to understand the terms, coverage options, and costs associated with different health insurance plans to select the most suitable coverage for one’s needs.

Health insurance is a type of insurance coverage that provides financial protection against medical expenses incurred due to illness, injury, or other health-related issues. It helps individuals and families manage the costs associated with healthcare services, including doctor visits, hospital stays, prescription medications, and preventive care.

Here are some key aspects of health insurance:

- Coverage for Medical Expenses: Health insurance policies typically cover a range of medical services, including hospitalization, surgery, diagnostic tests, prescription drugs, and preventive care (e.g., vaccinations, and screenings).

2. Premiums:

Policyholders pay premiums to the insurance company in exchange for coverage. Premiums may be paid on a monthly, quarterly, or annual basis, depending on the policy terms.

3. Deductibles:

Health insurance policies often include deductibles, which are the amount of money the insured individual must pay out-of-pocket before the insurance company begins to cover expenses. Higher deductibles typically result in lower premiums, while lower deductibles usually mean higher premiums.

4. Copayments and Coinsurance:

In addition to deductibles, policyholders may be responsible for copayments (fixed amounts) or coinsurance (percentage of costs) for certain medical services. These costs are usually paid at the time of service.

5. Networks:

Health insurance plans may have networks of healthcare providers, including doctors, hospitals, and specialists, with whom they have negotiated discounted rates. Policyholders may pay less for services received from in-network providers compared to out-of-network providers.

6. Preauthorization:

Some health insurance plans require preauthorization or prior approval for certain medical procedures, treatments, or medications to ensure they are medically necessary and covered by the policy.

7. Coverage Limits and Exclusions:

Health insurance policies may have coverage limits, such as annual or lifetime maximums, on certain benefits. Additionally, they may exclude coverage for specific services, treatments, or pre-existing conditions.

8. Prescription Drug Coverage:

Many health insurance plans include coverage for prescription medications, either through a formulary (list of covered drugs) or a tiered system with different copayment amounts for generic, brand-name, and specialty drugs.

9. Preventive Care Services:

The Affordable Care Act (ACA) requires health insurance plans to cover certain preventive care services, such as vaccinations, screenings, and counseling, without requiring copayments or deductibles.

10. Marketplace and Employer-Sponsored Plans:

Health insurance coverage can be obtained through government-run marketplaces (e.g., Healthcare.gov in the United States) or through employer-sponsored plans, where employers provide health insurance benefits to their employees as part of their compensation package.

Property Insurance

Property insurance is essential for protecting individuals, families, and businesses from financial losses associated with property damage or loss. It’s important to carefully review policy terms, coverage options, exclusions, and limitations to ensure adequate protection for valuable assets.

Property insurance is a type of insurance that provides financial protection against damage or loss to physical assets, such as homes, buildings, personal belongings, and vehicles. It helps individuals and businesses recover from unexpected events that may cause damage to their property, such as fires, natural disasters, theft, or vandalism.

Here are some key aspects of property insurance:

- Coverage for Physical Assets: Property insurance policies typically cover the cost of repairing or replacing damaged or lost property due to covered perils. This can include structures (e.g., buildings, homes), contents (e.g., furniture, appliances), and other personal belongings (e.g., clothing, electronics).

Types of Property Insurance Policies:

a. Homeowners Insurance: Protects homeowners against damage to their property and liability for injuries or property damage to others.

b. Renters Insurance: Covers the personal property of tenants renting a residence and provides liability coverage.

c. Commercial Property Insurance: Provides coverage for businesses’ buildings, equipment, inventory, and other physical assets.

d. Condo Insurance: Covers personal property and liability for condominium unit owners, typically in conjunction with coverage provided by a condo association’s master policy.

Landlord Insurance:

Protects landlords from financial losses related to rental properties, including property damage and liability claims.

Covered Perils:

Property insurance policies specify the types of perils or risks that are covered. Common covered perils include fire, lightning, windstorms, hail, theft, vandalism, and certain types of water damage. Some policies also offer optional coverage for additional perils, such as earthquakes or floods.

Policy Limits:

Property insurance policies have coverage limits, which represent the maximum amount the insurer will pay for covered losses. Policyholders need to review and understand their policy limits to ensure they have adequate coverage for their property.

Deductibles:

Property insurance policies often include deductibles, which are the out-of-pocket expenses the policyholder must pay before the insurance company begins to cover the remaining costs of a claim. Higher deductibles typically result in lower premiums.

Replacement Cost vs. Actual Cash Value:

Property insurance policies may provide coverage for property on a replacement cost basis, which covers the cost of repairing or replacing the damaged property with new items of similar kind and quality. Alternatively, coverage may be provided on an actual cash value basis, which takes depreciation into account when determining the value of the damaged property.

Additional Coverages and Endorsements:

Property insurance policies may offer additional coverages or endorsements to customize coverage based on the policyholder’s needs. Examples include coverage for valuable items (e.g., jewelry, artwork), identity theft, or loss of use (e.g., temporary living expenses if a home is uninhabitable).